Recently ranked by TechTimes as number one among the top five best Fintech events worldwide, the annual Sopra Banking Summit returns for its second edition. With more than 5,000 attendees already signed up, the event will envision the financial world of the future, by bringing together visionary market leaders covering three key themes: “Achieve operational efficiency,” “Engage your clients” and “Open up your ecosystem.”

“How open finance regulations will foster innovation” with Jan Ceyssens, Wijnand Machielse, Christian Schäfer, Cyril Armange and Bruno Cambounet

Here is our all-star list of panelists:

- Jan Ceyssens, Head of the Digital Finance Unit for the European Commission

- Wijnand Machielse, European Markets Director at SRC and Member of the Berlin Group

- Christian Schäfer, co-Chair of the SEPA Payment Account Access Scheme

- Cyril Armange, Deputy CEO of Finance Innovation

- Bruno Cambounet, Head of Research at Sopra Banking Software, and co-Chair of the Open Finance Advisory Board at the Berlin Group.

This session is a must-see for anyone interested in the role that open finance will play in the future of banking. By considering the PSD2 directive and its implementation across Europe, this session explores how the various initiatives in business, standardization and regulation can be combined to support the opening up of the financial ecosystem.

“75% of banks around the world are acknowledging the opportunity in collaborative models. A fifth of banks worldwide declare themselves ready for open finance. And progress has been made across various fronts in Europe.” – Bruno Cambounet

Jan Ceyssens, member of the European Commission, speaks about the potential of open finance & open data in Europe in the coming years:

“PSD2 has really grown this year – not only within the financial sector but also for the economy at large. We have – on the Commission side, in our data strategy for Europe – recognized this potential for data sharing and data-driven innovation. These two things really need to go hand-in-hand in Europe.

“In Europe, we have an economy which is not marked by very large players but a lot of players, and in that sense, to leverage innovation and the data economy, you need to share data, otherwise it would not be possible. So, in that sense, I think the objective of data sharing and thereby improving the economy – making, creating innovative products – is essential for Europe. And that sharing needs to happen within certain sectors but also beyond those sectors.”

On the question of regulation, Jan says that coordination with key stakeholders is vital, putting in place a system that ensures that data can flow freely while also maintaining trust from the end-users.

Do you want to find out more about this topic? The session’s on-demand replay is available here.

“Add artificial intelligence to your bank, today!” with David Lejolivet, Mohammed Sijelmassi and Dana Lunberry

Artificial intelligence and machine learning-based solutions now represent the future for many industries, and banking is undoubtedly one of them. Financial institutions are now on the lookout for solutions that allow them to provide the best customer experience and to streamline their business processes, while reducing their operational costs and improving their products and services.

This session provides the perfect opportunity to find out more about the role of artificial intelligence in banking, but also to showcase Sopra Banking Software’s latest Core Banking solution around AI and machine learning, through proven use cases and demos.

Dana Lunberry, head of data strategy at Sopra Banking Software, starts the session by sharing a few key numbers on AI:

- Global AI in the banking market is expected to reach $64 billion by 2030

- 44% of the banking software market will be led by AI by 2027

- 50% of projects are already leveraging AI to improve customer experience.

“AI also helps institutions to boost productivity and lower their costs through more automation and a better use of resources. By processing large amounts of data, banks are finding new opportunities to delight their customers, with new and better products and services, and they are also finding new markets to serve.”

David Lejolivet, Sopra Banking Software’ solution offering director, continues the conversation by giving more details about how companies can use AI in their solutions:

“Sopra Banking Software focuses on bringing transformation on three aspects, called the three Es: efficiency, effectiveness, experience. Banks are using several IT systems, and all those systems used by customers generate lots of data. Using AI, a lot of intelligence could be implemented, using all that data. What is also important is that when we start processing all that data, it’s not only the data from your own system, it’s also data coming from your legacy, core solutions and external data to improve analysis.”

Here are a few examples of “intelligent banking” processed by AI on the Sopra Banking Platform:

- Customer churn prevention

- Portfolio credit risk enhancement

- Contract lifecycle optimization

- Payment automation

- Credit scoring and risk analysis

- Pricing and promotion analytics

- Customer claims.

Indranil Bandyopadhyay, principal analyst at Forrester, discusses the four themes central to the future of banking: invisible (where banks embed themselves into the client needs, which are not transactional in nature), connected (to the ecosystem, going beyond traditional banking), insight-driven (using data smartly) and purposeful (ESG analytics).

According to a Forrester study, banks are currently focusing on enhanced efficiencies and customer experience. They plan to use – or are already using – AI technologies to:

- Improve efficiency of IT operations (34%)

- Improve efficiency in business operations (33%)

- Gain better customer insights (33%)

- Improve data, analytics and insights platforms (32%)

- Improve business automation (25%).

When using AI technology, banks may achieve the following benefits: increase automation of internal processes (39%), increase safety (32%), improve security (32%). As well as the following challenges: lack of skills to implement and operate such systems (22%), lack of transparency of how AI/ML systems build models (22%), lack of skills to develop AI solutions (21%).

Do you want to find out more about this topic and Sopra Banking Software’s AI solutions? You can watch the session’s on-demand replay following this link.

“Sustainable & green financing: the new normal,” with Bettina Vaccaro Carbone, Graham Filmer and David Briggs

Green IT and sustainability are becoming hot topics for board level discussions across financial institutions. In this session, our expert speakers delve into how this has evolved in the auto finance industry.

Graham Filmer, director of Rocket Performance Group, opens the talk by sharing a few words about Environmental Social & Governance (ESG) and the future of car mobility.

“In automotive mobility, the implications environmentally of cars are having a huge impact on the cars we will all drive in the next few years. In the UK, from 2030, all internal combustion engine cars will not be allowed to be sold. And 2035 will be the end of hybrid cars as well. We’re already on that journey and it will be a massive change for everybody.”

But why does the market need a green lender? David Briggs, managing director of Tandem Motor Finance, shares his insights.

“We’re focusing on how we can influence UK consumers in making greener choices in the future. The production and sale of internal combustion engines is soon coming to a finish, and EVs (electric vehicles) will be much more dominant in the marketplace. But there’s much more to our approach than simply financing EVs.

“Equally important is how we finance and how we lend. We are committed to providing banking for a greener future, and we want to be recognized as a business that is committed to helping people and businesses to make that transition to a greener future.”

When it comes to financing green products, David says that it starts with cars, but that it can be extended to light commercial vehicles (LCVs), motorcycles and other modes of transport. He goes on to say that the two aspects to consider are digitization and sustainability.

“The key to it is to put the two pieces together, sustainable digitalization, and the companies that achieve that and get that right will be the ones that will retain customers and grow their customer base.”

Do you want to find out more about green financing and sustainability in the automotive industry? Watch the session’s on-demand replay by clicking on this link.

“Financial inclusion & microfinance: how to run at scale,” with David Lejolivet, Nelly Kambiwa and Mahmoud Drissi

Financial inclusion is a major topic for everyone around the world. And it’s at the heart of Sopra Banking Software’s strategy.

This session considers the potential of financial inclusion, as well as its opportunities in the African market. It also showcases Sopra Banking Sotfware’s platform for Financial Inclusion, which brings a comprehensive response to the pain points encountered by financial institutions in delivering inclusive financial products and services to the right populations.

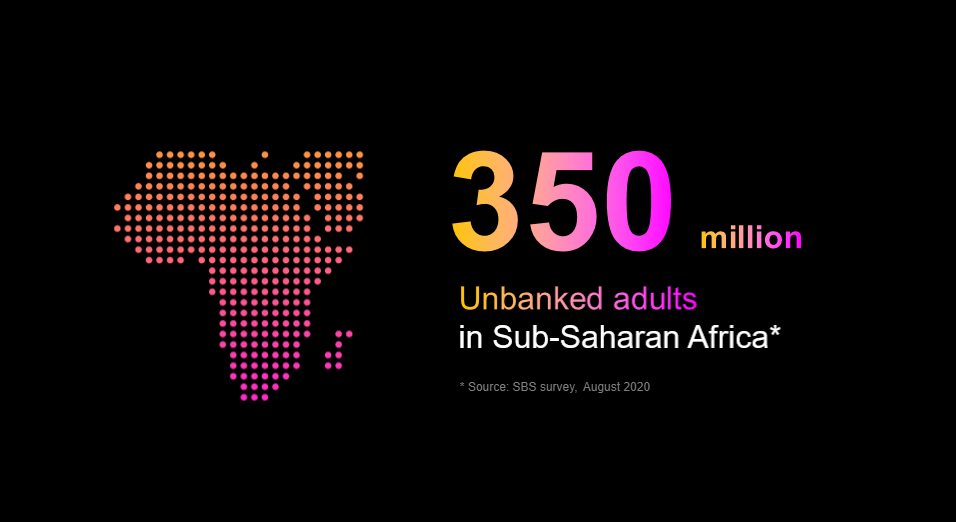

Nelly Kambiwa, Financial Inclusive Director at Sopra Banking Software, kicks off the session by talking about the financial inclusion market in Africa, delivering an astounding figure: 350 million unbanked adults are currently living in sub-Saharan Africa, representing nearly two-thirds of the total African population.

These people don’t have access to basic banking services, such as:

- Opening a bank account

- Managing money transfer

- Applying for a bank loan.

Furthermore, only 20% of African households have a bank account, representing one fifth of African households. This can be explained by the fact that 65% of the African population live in rural locations and live far away from large cities. According to Nelly, “At Sopra Banking Software, we want to address through our technologies the financial inclusion players that will respond to the unbanked people needs.”

Those players can be traditional organizations, such as micro-finance institutions and banks, but also neobanks or telecoms operators. They have all been impacted by three main drivers:

- The government and regulator initiatives pushing financial inclusion

- The speed of digital use cases around financial inclusion

- The boom of the African fintech market (+60% the two last years).

David Lejolivet, Head of Solution Offerings at Sopra Banking Software, continues the conversation by stating that 30 million people are benefiting from the company’s financial inclusion solutions, which facilitate their daily lives and help them in their business development.

It’s equally important to note that there’s more than one way to address financial inclusion initiatives, and that there are diverse kinds of institutions. To be able to run financial inclusion at scale, a few requirements are needed:

- API-first financial inclusion

- Full financial products

- Omnichannel operations

- Fully automated processes.

Sopra Banking Software has more than 100 modules covering business, compliance and regulation.“It means that for institutions choosing our solution, it is possible to start small, activating only a few features to fulfill their strategy. Progressively, if they want to change their business model a little bit, enhance business cases or the way they would like to apply the efficiency of the bank, they can activate additional modules just by configuration, in complete autonomy. It’s not something that will evolve, and this way we accompany the evolution of the financial institutions.”

Currently, Sopra Banking’s financial inclusion platform is deployed in more than 20 countries in Africa, with more than 30 customers.

Are you interested in learning more about financial inclusion? If yes, you can watch the session’s on-demand replay by clicking on this link.